Three powerful dynamics unfolding in the global economy are expected to play a significant role in investors’ multi-asset allocations over the next five years, according to a 132-page report from Rotterdam-based asset manager Robeco.

The first is labor’s likely increased bargaining power, with the outcome of any tussle between businesses and their workers probably being determined by wages in a sticky inflation environment, based on the report compiled by strategists Laurens Swinkels and Peter van der Welle on behalf of the multi-asset team at Robeco, which manages $194 billion in assets. The second is the end of monetary-policy leniency and the potential for central banks to lock “horns” with governments over the appropriate level of borrowing costs. The third is the dawn of “multipolarity” as the U.S. and China struggle for power.

Taken together, this “triple power play” is already starting to unfold, shifting investors into a world of higher risk-free rates and lower expected equity risk premiums, according to the asset manager. Risk premium is a gauge of relative value for stocks, helping investors understand what their short-term gain might be when taking on the additional risk of buying equities or investing in stock funds.

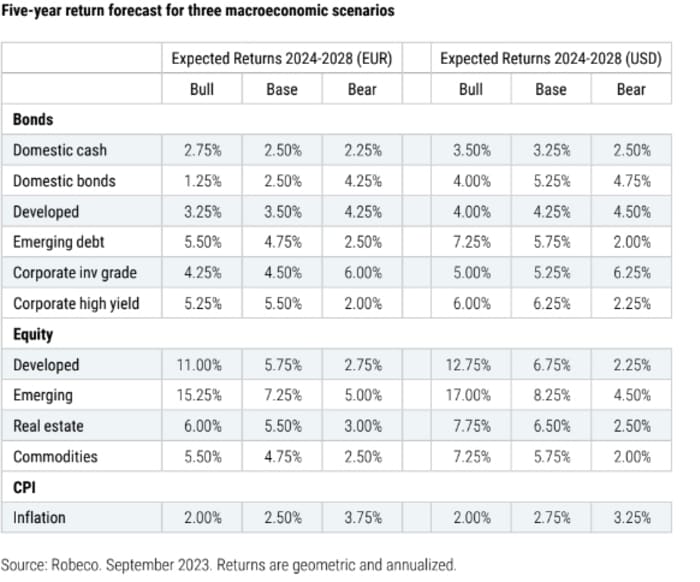

Robeco provided its forecasts for five-year annualized, projected returns on a range of assets held by euro- and dollar-based investors — including developed- and emerging-market equities, bonds, and cash.

The firm’s base-case scenario, which Robeco’s team refers to as a “stalemate,” calls for a mild recession in 2024, consumer-price inflation in developed economies to remain around 2.5% on average heading toward 2029, and real GDP in the U.S. to average 2.3% or below what the S&P 500 index

SPX

currently implies.

That benign growth outlook is expected to be accompanied by macroeconomic volatility, plus a “tug of war” between central bankers reluctant to lower interest rates and governments in need of low borrowing costs — which “means there is not enough monetary policy tightening to remove demand-pull inflation.” Under such a scenario, developed-market equities are likely to underperform their emerging market counterparts and domestic bonds should offer a higher return than cash for dollar-based investors, according to Robeco.

Source: Robeco. Returns shown are annualized.

“Looking ahead, a key question is: are we eyeing the start of a new bull market that will broaden and pave the way for another streak of above-historical excess equity return?” the Robeco team wrote in the report released on Tuesday. “In our base case, we expect developed markets’ earnings growth to end up below current 5Y forward consensus projections, which are high single-digit or even still low double-digit for the U.S. and eurozone.

“The reason we foresee a decline in profitability is linked to our overarching macro theme, the triple power play. Equities will likely bear the brunt of the power play in geopolitics,” according to the report. In addition, efforts by global corporations to shift production toward geopolitically-friendly powers or closer regions “will prove more costly and lower efficiency.” Plus, “further pressure from margins will come from a lagged response from past policy rate hikes.”

Under Robeco’s bull-case scenario, early and rapid adoption of artificial intelligence across sectors and industries would likely spawn above-trend growth and push inflation back to central banks’ targets. The result is “an almost Goldilocks scenario in which things are running neither too hot nor too cold,” central banks could take a break from tightening policy, and developed- and emerging-market equities may both be able to come out with double-digit annualized returns from 2024 to 2028.

The firm’s bear-case scenario envisions a world in which mutual trust between the world’s superpowers hits rock bottom, governments are “in the crosshairs” of central banks, and labor loses bargaining power in the services sector. A “stagflationary environment emerges, intensifying the policy dilemma for central bankers” as inflation stays stubbornly high at 3.5% on average and growth comes in at just 0.5% annually for developed economies. In that situation, developed-market equities would eke out an annualized return of 2.25% for dollar-based investors over the four-year period that’s below the expected return on cash.

On Thursday, all three major U.S. stock indexes

DJIA

COMP

were higher as investors digested a batch of better-than-expected U.S. data and continued to expect no action by the Federal Reserve next week. Officials are seen as likely to leave their main policy rate target at a 22-year high of 5.25%-5% on Wednesday.

Meanwhile, Treasury yields were mixed and the ICE U.S. Dollar Index jumped 0.6% as investors also monitored the possibility of a strike by United Auto Workers. In a separate development earlier this week, Air Force Secretary Frank Kendall warned that China is preparing for a potential war with the U.S.